|

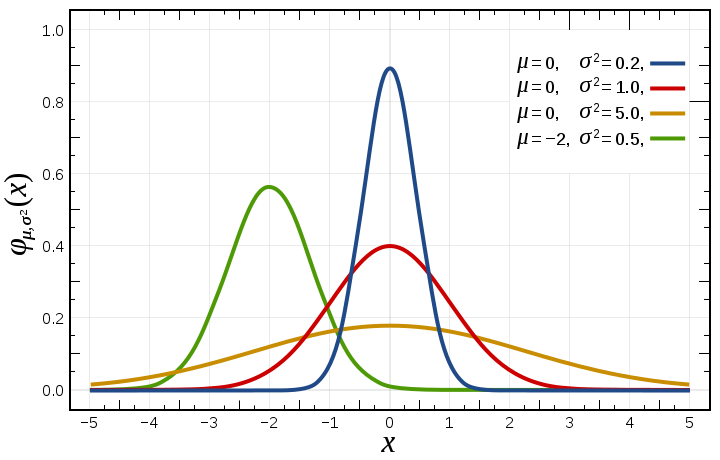

| Probability density function for the normal distribution (Image Source : Wikipedia) |

Definition:

A random variable X is defined to be normally distributed if its density is given by

Where new satisfies -infinity<x<+infinity and sigma>0 is called a normal distribution.

The symbols used new and sigma square to represents the parameters. Where new is mean of the distribution and sigma square is the variance of the distribution.

No comments:

Post a Comment

Statistics becomes simple when we share and discuss. Drop your questions or suggestions below — I’ll be happy to respond!